How long does CIBIL take to update after payment?

If you’ve just cleared a credit card overdue or finally paid off that personal loan EMI you missed, the first thought that comes to mind is simple: “When will my CIBIL score improve?”

I’ve handled credit reviews for borrowers for over 15 years — retail loans, SME cases, credit restructuring, settlements, you name it. And I can tell you this confidently: most people misunderstand how CIBIL updates actually work.

They assume the moment payment is made, the score should jump within a day or two.

That’s not how the system functions.

Let’s break this down properly — with real timelines, real banking processes, and what actually happens behind the scenes in India.

Before we go deeper, let’s clearly answer the core question: how long does CIBIL take to update after payment in a typical Indian banking cycle?

What Is CIBIL and How Does It Update?

TransUnion CIBIL is India’s largest credit bureau. Banks and NBFCs report your loan and credit card data to CIBIL every month. Your credit score (ranging from 300 to 900) is calculated based on that data.

Important thing to understand:

CIBIL does not update your score instantly after you pay.

It only updates when the lender reports fresh data.

That reporting cycle is the real key.

Quick Answer:

In most cases, CIBIL takes 30–45 days to update after payment because lenders report credit data in monthly batches, not in real time. Faster updates are rare and usually depend on early reporting by the bank.

Standard Timeline: How Long Does CIBIL Take to Update After Payment?

In most cases:

30 to 45 days from the date of payment. This 30–45 day CIBIL update time is standard across most major Indian banks and NBFCs.

Here’s why.

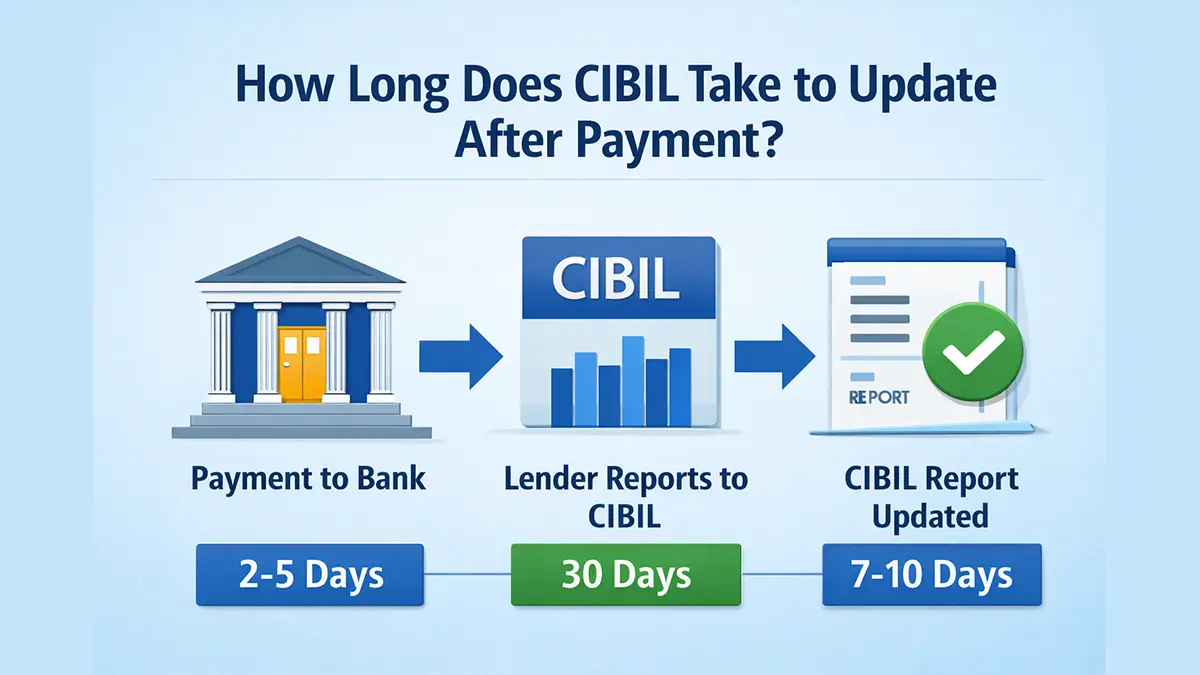

Step-by-step process (what actually happens):

- You make the payment (say, 10 January 2026).

- The bank updates its internal loan system.

- The bank closes its monthly reporting cycle (usually end of month).

- Data is submitted to CIBIL.

- CIBIL processes the batch and refreshes your credit file.

So if you pay on 10 January:

- The bank may report by 31 January.

- CIBIL may reflect it between 5–20 February.

That’s why it typically takes one full reporting cycle.

Real Borrower Example (Personal Loan EMI Case)

Let’s say:

- EMI due: ₹18,500

- Missed EMI in December 2025

- Paid overdue + penalty on 8 January 2026

Now here’s what usually happens:

- Bank marks December as “DPD 30” (Days Past Due)

- January payment clears overdue

- Bank reports updated status in end-January batch

- CIBIL reflects update mid-February

In practical terms, this means the CIBIL update after EMI payment usually follows the lender’s monthly reporting batch rather than the actual payment date.

Score improvement? Possibly.

But the DPD record for December stays in history.

And this is where many borrowers get confused.

Does CIBIL Remove Late Payment After You Pay?

No.

This is critical.

If you missed a payment and later cleared it, the record remains in your credit history for up to 36 months (sometimes longer depending on reporting).

However:

- The status changes from “Overdue” to “Closed/Regular”

- Your current standing improves

- Future lenders see that you regularized the account

In my experience, one isolated 30-day delay won’t permanently damage your profile — but repeated delays absolutely will.

Credit Card Payment Case – Different Timing?

Credit cards sometimes update slightly faster than loans because:

- Card cycles are monthly

- Reporting is automated

- Some banks report mid-cycle

Example:

- Credit card outstanding: ₹52,000

- Paid in full on 3 March

- Statement date: 15 March

- Bank reports on 31 March

- CIBIL updates by mid-April

But don’t expect score change within a week.

Even though the payment clears quickly, the CIBIL score update after payment still depends on when the lender submits fresh data.

That rarely happens in India.

Loan Closure: How Long Does CIBIL Take to Update After Full Loan Payment?

If you close a loan completely, timeline is similar:

30–45 days

But here’s something important.

In my lending experience, banks sometimes take longer to mark “Closed” status internally — especially older accounts or manually processed closures.

If you:

- Closed loan on 5 February

- Bank reports only in March batch

- CIBIL reflects by late March

That’s still normal. Many borrowers ask how many days CIBIL takes to reflect full loan closure, and the realistic answer remains within the same 30–45 day reporting window.

If it crosses 60 days, then you should follow up.

Settlement vs Full Payment – Major Difference

This is where borrowers make costly mistakes.

If you settle a loan for less than total outstanding (say ₹80,000 against ₹1,20,000), the account status becomes:

“Settled”

Not “Closed”

That stays in your report and impacts future loan approvals heavily.

Even after it updates, your score may not recover properly.

In 2026 lending environment, most major banks:

- Reject home loans if any recent “Settled” account exists

- Ask for No Dues Certificate + explanation

Payment timing is one thing.

Settlement impact is another.

Why Your CIBIL Score May Not Increase Immediately

Many borrowers expect a big jump after clearing dues.

Here’s reality.

Score depends on:

- Payment history (35% weight)

- Credit utilization

- Loan mix

- Credit age

- Enquiries

If your score was 650 due to multiple missed EMIs, paying one overdue EMI won’t push it to 750 instantly.

It improves gradually as:

Even if you understand how long does CIBIL take to update after payment, score recovery itself follows a longer behavioral pattern.

- Regular payments continue

- No new delays occur

- Utilization drops

In my advisory work, I usually tell clients:

Give it 2–3 clean reporting cycles before expecting meaningful improvement.

When Does CIBIL Update Faster?

Rare but possible in these situations:

- Bank manually pushes corrected data

- You raise dispute and lender responds quickly

- System reporting error gets corrected mid-cycle

Even then, it usually takes at least 15–20 days.

Instant updates? No.

Even in accelerated cases, the update timeline still depends on whether the lender pushes corrected data within the same reporting cycle.

How to Check If CIBIL Has Updated

You can check via:

If you’re checking because you’re wondering how long does CIBIL take to update after payment, remember that updates only reflect after the lender’s monthly data submission.

- CIBIL official website

- Banking apps that show credit score

- Third-party platforms

But small advice from experience:

Check only after 30 days.

Checking too early only increases anxiety.

What If CIBIL Is Not Updated After 45 Days?

Now we move to problem cases.

If:

- You paid on 1 January

- By 15 March it’s still showing overdue

Then do this:

- Contact bank’s customer care

- Request reporting confirmation

- Ask for updated statement

- If unresolved, raise dispute directly with CIBIL

In 90% of cases, delay is on lender side, not CIBIL.

Banks report updated credit data to TransUnion CIBIL every month as part of their standard reporting cycle. According to the official CIBIL dispute resolution framework, updates reflect only after lenders submit revised data to the bureau.

Myth vs Reality

Myth: CIBIL updates instantly after payment.

Reality: Updates happen only after lender reports monthly data.

Myth: Paying overdue removes late history.

Reality: Late history remains, but status changes.

Myth: Paying full loan immediately boosts score by 100 points.

Reality: Score change depends on overall credit profile.

Practical Tips From 15+ Years in Credit Advisory

Let me give you advice I usually give serious borrowers.

- Always pay 3–5 days before due date. Banks report based on due date, not payment clearance time.

- If closing loan, collect No Dues Certificate immediately.

- Avoid loan settlement unless absolutely unavoidable.

- Keep credit card utilization below 30%.

- Don’t apply for multiple loans while waiting for update.

- Track DPD column carefully in your credit report.

Small discipline beats panic corrections later.

Frequently Asked Questions

How long does CIBIL take to update after EMI payment?

Typically 30–45 days. That’s the standard answer to how long does CIBIL take to update after payment or after an EMI is cleared.

Will my CIBIL score increase immediately after clearing overdue?

Not immediately. Improvement reflects after next reporting cycle and depends on your overall credit profile.

Does CIBIL update on weekends?

No. Updates depend on lender data submission, not daily processing.

How long does CIBIL take to update after loan closure?

Normally 30–45 days. In some cases up to 60 days.

Can I request faster CIBIL update?

You can request lender to report early, but most banks follow fixed monthly cycle.

If I pay credit card bill today, when will it reflect?

Usually next statement cycle reporting — around 30 days.

Does part-payment update faster?

No. Reporting cycle remains same regardless of payment type.

Final Advisory Perspective

Here’s something I’ve observed repeatedly over the years.

Borrowers worry too much about when CIBIL updates, and too little about why the score dropped in the first place.

To summarize clearly: how long does CIBIL take to update after payment? In most Indian banking cases, expect one full reporting cycle — usually 30 to 45 days. That timeline is normal, not a delay.

Credit scoring in India isn’t about one payment. It’s about behavior patterns.

One missed EMI can be repaired.

Three months of irregularity creates long-term credibility concerns.

If you’ve paid your dues — good. That’s step one. Now focus on maintaining 6–12 months of clean repayment behavior. That’s what rebuilds trust with lenders.

If you’re actively working on rebuilding your profile, here’s a detailed guide on how to increase CIBIL score fast with practical, real-world strategies.

CIBIL updates are mechanical.

Credit reputation is behavioral.