If you work closely with students and middle-income families in India, you already know this: scholarship money isn’t “extra support.” For many households, it’s the difference between continuing education and dropping out quietly.

Every year, I see parents take short-term loans at 18–24% interest just to pay school or college fees while waiting for scholarship credits. Most don’t even know how the UP Scholarship process actually works. They just apply, wait, and hope.

URGENT UPDATE (Feb 17, 2026): If you made corrections to your 2025-26 scholarship form during the recent window, you must submit the printed hard copy to your college by February 18, 2026. This is a mandatory step for physical verification. Without this, your application will be rejected at the institutional level.

Let’s clear that confusion.

This detailed guide on UP Scholarship 2026 covers the last date, eligibility criteria, status check process, renewal updates, and common mistakes — explained in practical, real-world terms.

What Is UP Scholarship 2026?

It is administered through the Social Welfare Department of Uttar Pradesh via the official scholarship portal. and funds are disbursed through the Direct Benefit Transfer (DBT) system.

The UP Scholarship is a financial assistance scheme run by the Uttar Pradesh Government to support students from economically weaker and socially disadvantaged backgrounds.

It generally covers:

- Pre-Matric (Class 9–10)

- Post-Matric (Class 11–12)

- Undergraduate (BA, BSc, BCom, etc.)

- Postgraduate (MA, MSc, MCom)

- Professional Courses (Engineering, Medical, Management, etc.)

The objective is simple: reduce financial pressure so students can complete their education.

But the implementation is where timing, documentation, and verification matter more than most people realize.

UP Scholarship 2026: Important Dates (Expected Timeline)

While official dates are announced each academic cycle, based on previous academic cycles and notification trends, here’s what typically happen.

UP Scholarship Official Dates (2025-26 Cycle):

• Online Correction Window: Closed on February 13, 2026

• Hard Copy Submission to College: February 18, 2026 (Last Date)

• Re-Scrutiny by NIC: February 19 – February 27, 2026

• Data Locking by District Committee: March 10, 2026

• Final Payment Disbursement (DBT): March 18, 2026

• Next Session (2026-27) Registration: Expected July 2026

In my experience, students who apply within the first 30–45 days face fewer technical issues. Last-week applications often run into server slowdowns or document mismatch problems.

And yes, I’ve seen students miss out simply because they waited till the last 48 hours.

UP Scholarship 2026 Eligibility Criteria

Eligibility for UP Scholarship 2026 depends on category, family income, domicile status, and academic progression. Each condition is verified at multiple levels, so accuracy in documentation is critical.

1. Domicile Requirement

The applicant must be a permanent resident of Uttar Pradesh. A valid domicile certificate may be required during verification.

2. Category-Based Eligibility

The scholarship is generally available to students belonging to:

- SC / ST

- OBC

- General (Economically Weaker Section – EWS)

- Minority communities

The exact scheme (Pre-Matric or Post-Matric) may vary depending on category and course level.

3. Income Criteria (Typical Thresholds)

Income limits may differ slightly depending on category and government notifications, but generally:

- General / OBC / Minority: Annual family income up to ₹2,00,000

- SC / ST: Annual family income up to ₹2,50,000

One common mistake I’ve seen repeatedly is income certificate validity.

For example, if your income certificate expired in March 2026 and you apply in September 2026 using the old certificate, your application may be rejected during district-level verification.

Income limits and timelines are subject to official notification changes. Students should verify details on the official portal before final submission.

Always ensure your income certificate is valid for the current financial year before submitting the form.

4. Academic Requirement

The student must:

- Be enrolled in a recognized institution

- Have passed the previous academic year

- Maintain required attendance as per institutional rules

Backlogs in professional courses do not automatically disqualify a student. However, repeated academic failures or year gaps can create complications during verification and may lead to rejection in certain cases.

How Much Scholarship Amount Can You Expect?

Amounts vary depending on course type and category.

Typical support includes:

- Tuition fee reimbursement

- Maintenance allowance

- Hostel allowance (if applicable)

From practical cases I’ve handled:

- Class 9–10 students may receive ₹3,000–₹5,000 annually.

- Undergraduate students in government colleges may receive ₹8,000–₹12,000.

- Engineering/medical students can receive ₹25,000–₹60,000 depending on fee structure.

Keep in mind: reimbursement often depends on actual fee receipts uploaded.

If your college charges ₹42,000 but you upload receipt for ₹28,000, reimbursement will match documented fees.

How to Apply Online for UP Scholarship 2026

The scholarship is processed under the Direct Benefit Transfer (DBT) system, meaning funds are transferred directly to the student’s Aadhaar-linked bank account.

Broad process:

- Register as a new student (or renewal).

- Fill personal, academic, and bank details.

- Upload required documents:

- Aadhaar

- Income certificate

- Caste certificate

- Fee receipt

- Marksheet

- Submit application.

- Print form and submit to institution for verification.

Students can apply online through the official UP Scholarship portal here: Official UP Scholarship portal

One major issue I frequently see: bank account mismatch.

If the Aadhaar name is “Rahul Kumar” and the bank account shows “Rahul K,” the system may flag it. Always ensure exact matching.

UP Scholarship 2026 Status Check Online Process

Students can complete the UP Scholarship 2026 status check by registration number directly on the portal dashboard.

Check official UP Scholarship status here

Scholarship Status 2025-26 : Coming Soon

What Your UP Scholarship Status Means:

• Pending at Institute Level: Your college has your form but has not verified it in the system yet.

• Scrutiny Result (Suspect): Mismatch found in marks, income, or caste details; requires immediate verification.

• Verified/Recommended by District Scholarship Committee: Your form is approved and ready for payment.

• Sent to PFMS: The government has initiated the money transfer to your Aadhaar-linked bank account.

• Payment Date: Approved students can expect credits on March 18, 2026.

UP Scholarship 2026 Status Check: How It Actually Works

Most students check status repeatedly without understanding what each stage means.

Here’s how it moves:

- Application Submitted

- Forwarded by Institution

- Verified by District Welfare Officer

- Approved

- Payment Sent to Bank

- Payment Credited

If your status is stuck at “Forwarded by Institution” for weeks, usually the college hasn’t completed verification in bulk.

I’ve seen cases where colleges delay verification because internal audits are pending.

You can check status using your registration number and date of birth on the official portal.

Real-World Scenario: Why Timing Matters

Let me share a typical situation.

In September 2025, a BSc student from Kanpur applied on the final day. His income certificate was issued in April 2024 and expired in March 2025. He assumed it was still valid.

District verification rejected it in January 2026.

Result?

No scholarship credit. He had to take a ₹30,000 private loan at 20% interest to cover hostel dues.

That’s the financial cost of a documentation oversight.

Renewal vs Fresh Application: Important Difference

Many students assume renewal is automatic. It isn’t.

Renewal applicants must:

- Log in using previous registration ID.

- Update academic progression.

- Upload current year fee receipt.

- Ensure no academic gap.

If you skip renewal and try fresh registration, duplication may cause rejection.

I recommend setting a reminder every July to check portal activation.

Common Reasons for Rejection

Over 60% of rejection cases I’ve reviewed fall into predictable patterns:

- Bank account not linked with Aadhaar

- IFSC code incorrect

- Income certificate mismatch

- College code entered incorrectly

- Duplicate application

- Incomplete verification by institution

One overlooked factor: joint bank accounts.

Scholarship amount must usually be credited to the student’s individual account. Joint accounts sometimes trigger delays.

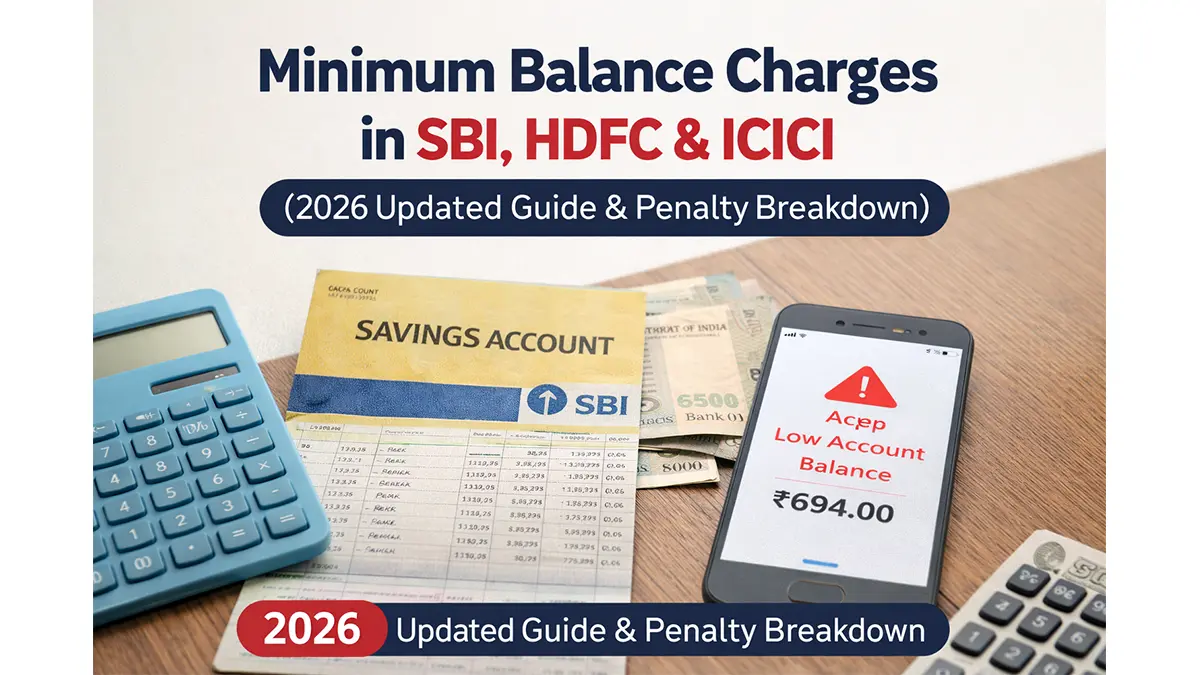

Also ensure your account maintains the required balance to avoid unnecessary deductions. You can check the latest minimum balance charges in India 2026 across major banks.

Myth vs Reality

Myth: If you submit the form before the last date, you are safe.

Reality: Submission is only step one. Verification stages matter more. Delays at institute or district level can still result in rejection.

Financial Impact of Delay in Scholarship Credit

Most families underestimate cash flow impact.

If a college demands ₹25,000 by December and scholarship credit comes in February, families either:

In many cases, delayed payments lead to missed instalments on existing loans. If you’re worried about penalties and credit impact, read our detailed guide on missed loan EMI in India and its consequences.

- Borrow informally

- Use credit cards

- Delay fee payment (risking exam hall ticket)

In middle-class households earning ₹18,000–₹25,000 per month, this gap creates stress.

My advice: never depend solely on expected scholarship for immediate fee deadlines.

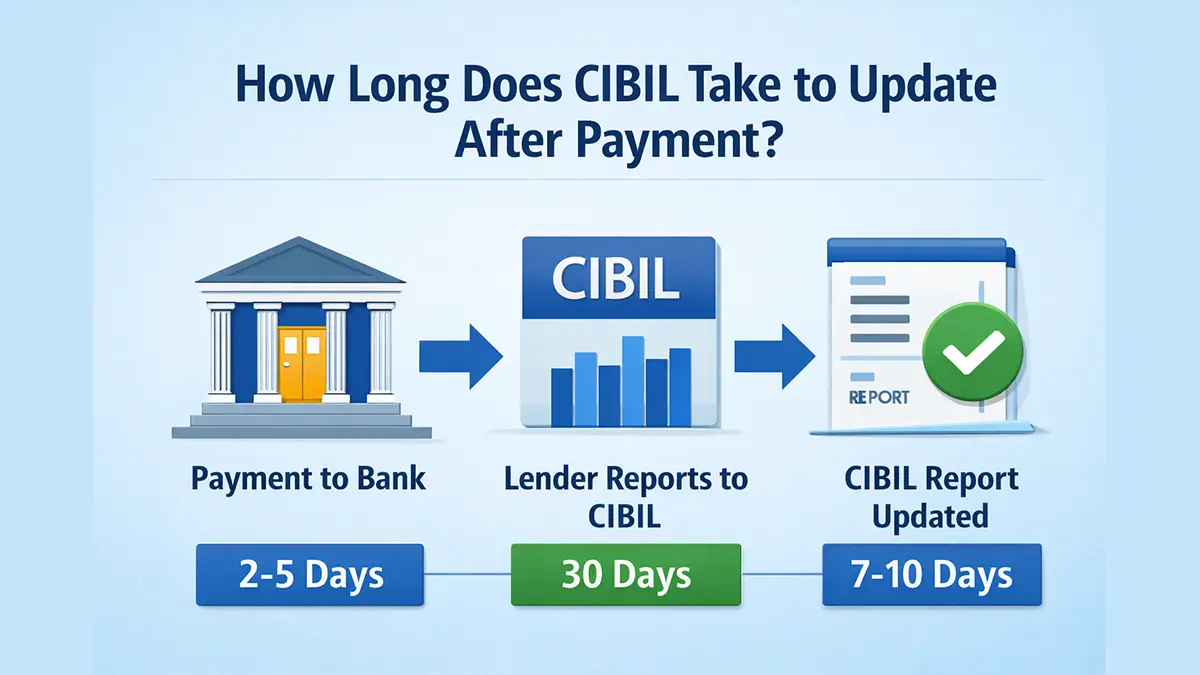

If scholarship money gets delayed, some families use short-term borrowing, which can impact their credit profile. You can understand how credit score updates work in detail in our guide on how long does CIBIL take to update after payment.

Practical Tips (From Experience)

- Apply within first month of portal opening.

- Cross-check bank details twice.

- Upload clear scanned documents — blurred uploads cause silent rejections.

- Follow up with college clerk after submission.

- Track verification stage monthly.

- Keep soft copies stored safely.

Small diligence prevents big financial problems.

Latest Updates for 2026 (Expected Trends)

Based on previous policy adjustments:

- Increased digital verification through Aadhaar linking.

- Stronger income certificate validation.

- Faster DBT (Direct Benefit Transfer) processing in public sector banks.

- Tighter scrutiny for professional course fee claims.

Digital audits are becoming stricter. Documentation must be clean.

When Will UP Scholarship 2026 Money Be Credited?

Many students also search for “UP Scholarship 2026 kab aayega” — typically, payment is released only after district-level verification is completed.

Based on previous cycles, UP Scholarship 2026 payments are typically credited between January and March 2026 after district-level verification is completed. However, delays may occur due to document mismatches, bank validation issues, or institutional verification backlog.

If your application status shows “Approved” but payment is not received within 30–45 days, first verify your Aadhaar-bank linking and IFSC details. In some cases, students borrow temporarily and worry about their credit profile. You can read our detailed guide on how long CIBIL takes to update after payment for clarity.

Frequently Asked Questions (FAQs)

What is the last date for UP Scholarship 2026?

The last date for corrected hard copy submission for the 2025-26 cycle is February 18, 2026. Fresh registrations for the 2026-27 cycle are expected in July 2026.

Can students from private colleges apply?

Yes, if the institution is recognized and listed on the scholarship portal.

How long does it take to receive scholarship money?

Typically 3–5 months after application submission, depending on verification stages.

What if bank details are wrong?

Application may be rejected or payment may fail. Correction window must be used carefully.

Can final-year students apply?

Yes, if enrolled during academic year and meeting eligibility criteria.

Is Aadhaar mandatory?

In most cases, yes — especially for DBT credit processing.

Can I edit my application after submission?

Only during official correction window.

UP Scholarship 2026 Last Date: Final Reminder

The official UP Scholarship 2026 last date is expected between October and November 2026. However, students are strongly advised not to wait until the final week to submit their application.

Final Advisory Insight

Scholarships are not charity. They are structured financial support systems. But like every government-linked financial mechanism in India, they require procedural discipline.

In my years of advising families, I’ve seen this pattern: the students who treat the scholarship like a formal financial process — not just an online form — rarely face rejection.

Track dates. Maintain documents. Follow up actively.

Education funding in India is becoming increasingly digitized. That’s good news — but only for those who stay organized.

If you approach UP Scholarship 2026 with clarity and timeliness, it can significantly reduce your financial burden.